By Wade D. Pfau, Ph. D., CFA, RICP

Comparing guaranteed lifetime withdrawal benefit riders within variable annuities

Executive summary

More Americans are interested in generating guaranteed income in retirement. In fact, LIMRA research shows there has been an increase in workers' willingness to convert assets into lifetime-guaranteed income, which has increased 14 percentage points from 38% in 2017 to 52% in 2023.1 Variable annuities, when annuitized, are one solution available to generate guaranteed income. Variable annuities may also offer an income rider, such as a guaranteed lifetime withdrawal benefit (GLWB), which offers guaranteed income for the lifetime of the contract holder for an additional cost without the loss of control over the annuity contract value that occurs when an annuity contract is annuitized. Annuitization is an irreversible commitment to converting an annuity contract into a series of payments, and GLWBs provide a method for constructing guaranteed lifetime withdrawal amounts while maintaining flexibility to end the payments.

This paper analyzes the hypothetical historical performance of MassMutual EnvisionSM variable annuity with a GLWB called MassMutual RetirePaySM, compared to different variable annuities with a GLWB. Not all GLWB riders are the same. Some focus on growth of the benefit base, while others place an emphasis on the withdrawal rates.

The purpose of this analysis is to help financial professionals compare the benefits and constraints of the most popular designs of GLWBs to see which provide clients with the highest level of income. The variable annuities with GLWBs in this paper are based off the top-selling products in the marketplace today. Historical time periods, both bull and bear markets, were used to determine which GLWB structure would have provided the contract holder with the highest annual guaranteed income amount at different issue ages and deferral periods. This guaranteed lifetime income is key for determining which product is the best fit for clients.

Overall, the analysis suggests that RetirePay provides the most guaranteed annual lifetime income in many scenarios due to the higher withdrawal rate. It is important to note that RetirePay and traditional GLWB riders are retirement income solutions that fit different client needs and scenarios. Traditional GLWBs offer benefit base guaranteed growth using roll-ups. This might be best for someone who values guarantees or wants to plan with a guaranteed growth model, because the annual minimum increase to the benefit base is known regardless of market conditions. RetirePay takes a different approach by using a withdrawal rate that increases with the length of deferral, which creates a similar impact as a roll-up, offering the potential for higher lifetime income in longer deferral periods or in periods with strong market performance.

MassMutual has designed their GLWB to focus on the growth of the withdrawal rates compared to concentrating on the benefit base growth like most traditional GLWB designs. In instances where a client can wait 10 or more years, they enjoy a higher withdrawal rate for up to 10 years and they have more opportunity for market growth, which could result in a higher benefit base. These are both ways to support more guaranteed income for clients.

Want to learn more about retirement income solutions?

Explore our comprehensive resources on variable annuities and discover how to help your clients create sustainable retirement income streams.

Key product comparison

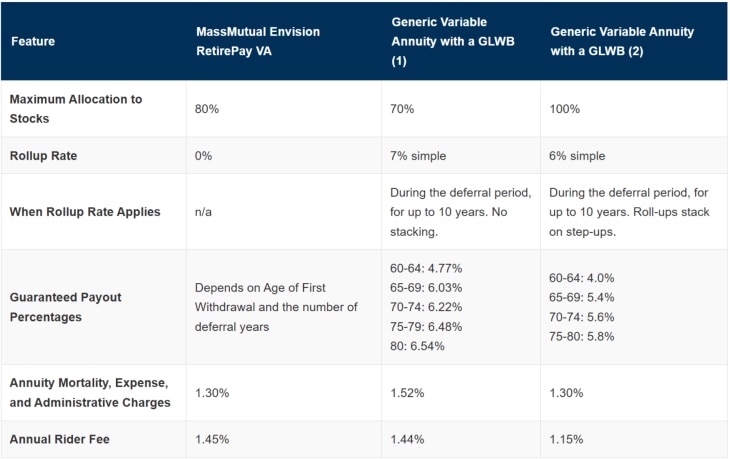

Understanding the differences between GLWB structures is essential for financial professionals. The following exhibit summarizes the key characteristics of MassMutual Envision with RetirePay compared to common GLWB designs in the marketplace.

Exhibit 1: Summarizing the variable annuities with a GLWB

Note: Underlying annual account fees of 0. 75% subaccount fee consistent across all annuities.

RetirePay's advantage: Rather than focusing on benefit base roll-ups, RetirePay emphasizes higher withdrawal rates that increase with deferral length. This design can provide more guaranteed annual lifetime income, especially when clients defer for 10 or more years.

Learn more about how MassMutual variable annuities can enhance your clients' retirement income strategies.

Historical performance analysis

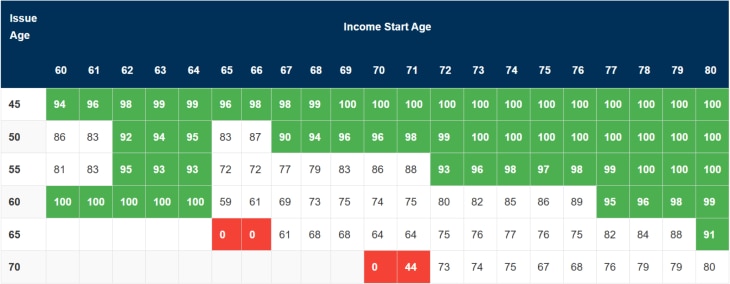

Using historical market data from 1871 to 2024, we analyzed how RetirePay performed against generic GLWB structures across various issue ages and income start ages. The results demonstrate when RetirePay is most likely to provide higher guaranteed income.

Exhibit 2: Probability that RetirePay offers more initial income than first generic GLWB

From rolling historical periods, 1871-2024.

Note: Green shading for success rates at 90% or greater; red shading for success rates 50% and below. White shading for success rates between 51% and 89%.

Key finding: RetirePay shows significantly higher likelihood of providing more guaranteed income in most age scenarios, particularly with longer deferral periods. The only exceptions are relatively shorter deferral periods before starting income at age 65 or 66.

Looking to compare retirement income solutions for your clients? Visit our sales ideas and concepts page for presentation materials and client discussion tools.

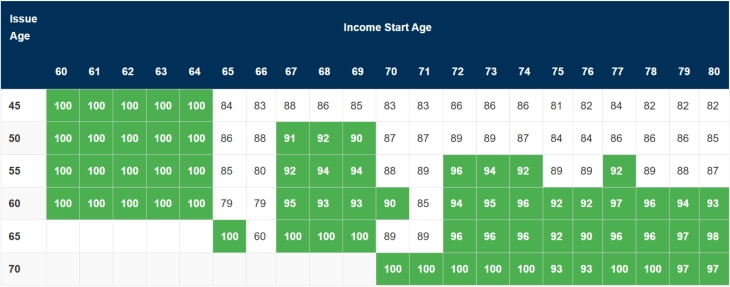

Exhibit 3: Probability that RetirePay offers more initial income than second generic GLWB

From rolling historical periods, 1871-2024.

Note: Green shading for success rates at 90% or greater; red shading for success rates 50% and below. White shading for success rates between 51% and 89%. It is the combination of roll-ups, step-ups, and withdrawal rates that combine to provide more guaranteed income.

Key finding: When compared to a GLWB with 100% equity allocation and stacking roll-ups, RetirePay remains competitive. While the generic GLWB benefits from higher equity exposure and stacking features during the first 10 years, RetirePay's higher withdrawal rates help it remain competitive, especially for clients at the analysis target ages (62, 67, and 72) where RetirePay is specifically designed to optimize income.

Want the complete analysis?

This blog post highlights key findings from Dr. Wade Pfau's comprehensive whitepaper. The full research includes detailed methodology, additional historical scenarios comparing bull and bear markets, in-depth technical analysis of GLWB mechanics, and complete data tables.

Download the complete 2025 whitepaper to access:

- Full methodology and assumptions

- Complete historical analysis (1871-2024)

- Detailed bull and bear market scenarios

- All exhibits and supporting data

- Technical appendices and calculations

Let's work together

Call us today to talk about how you can add dependability to your clients’ retirement strategies.

1-855-464-3436 Or, learn more about variable annuities from MassMutual.

Not a financial professional?

Visit MassMutual.com.

Let's work together

Call us today to talk about how you can add dependability to your clients' retirement strategies.

Or, learn more about variable annuities from MassMutual.

Not a financial professional?

Visit MassMutual.com.

FOR BROKER/DEALER USE. NOT FOR USE WITH OTHER AUDIENCES.

1 https://www.limra.com/en/newsroom/industry-trends/2023/are-in-plan-annuities-at-a-tipping-point/

The information provided in this white paper is not written or intended as specific tax or legal advice. MassMutual and its subsidiaries, employees, and representatives are not authorized to give tax or legal advice. individuals are encouraged to seek advice from their own tax or legal counsel.

This white paper is designed to provide information. It does not represent advice or a recommendation regarding a particular insurance product or to engage in or refrain from a particular course of action. The information within has not been tailored for any individual.

MassMutual is not affiliated with Wade Pfau and the American College of Financial Services.

MassMutual Envision (Contract Form FPVDA21 and ICC21-FPVDA in certain states, including North Carolina) is a flexible premium deferred variable annuity contract issued by Massachusetts Mutual Life Insurance Company, Springfield, MA 01111-0001.

The material is intended to compare MassMutual RetirePay to competitor GLWBs as of the date noted during the markets referenced (1982–1992, 1990–2000, 2009–2019). You should run an illustration to verify income amounts.

Variable annuities offered through registered representatives of MML Investors Services, LLC, Springfield, MA 01111-0001, or a broker-dealer that has a selling agreement with MML Strategic Distributors, LLC, Springfield, MA 01111-0001.

Principal Underwriters: MML Investors Services, LLC (MMLIS), Member SIPC, and MML Strategic Distributors (MSD). MMLIS and MSD are members of FINRA and subsidiaries of Massachusetts Mutual Life Insurance Company, Springfield, MA 01111-0001.

Any guarantees explicitly referenced herein are based on the claims-paying ability of the issuing insurance company.

MassMutual Envision with RetirePay and/or certain features and investment options may not be available in all states or firms.