Whole life insurance and the dividend

The dividend difference

A participating whole life insurance policy from MassMutual offers a variety of benefits, guaranteed death benefit protection, guaranteed level premiums, cash value accumulation, and income tax advantages, but it also offers the potential to receive policy dividends. While dividends are not guaranteed, MassMutual has paid them to eligible participating policyowners every year since 1869.

The eligibility to receive dividends is an important part of the overall value that MassMutual participating whole life insurance offers. Clients have several options for how they can elect to use any dividends they may be eligible to receive. They can elect to receive them in cash or choose an alternative dividend option including the following:

- Purchase paid-up additional whole life insurance

- Reduce the following year’s premium payment

- Purchase additional one-year term insurance

- Leave on deposit to accumulate with interest

- Repay a policy loan or pay loan interest

Whole life policy with paid-up additions (PUA)

The most commonly elected dividend option at MassMutual is paid-up additions (PUAs). With this option, any dividends received will purchase additional whole life insurance, which will also be eligible to receive future dividends. This helps clients grow their policy values over time, increasing the death benefit and cash value, which can be accessed1 when they and their loved ones need it most.

Case study: PUAs in action

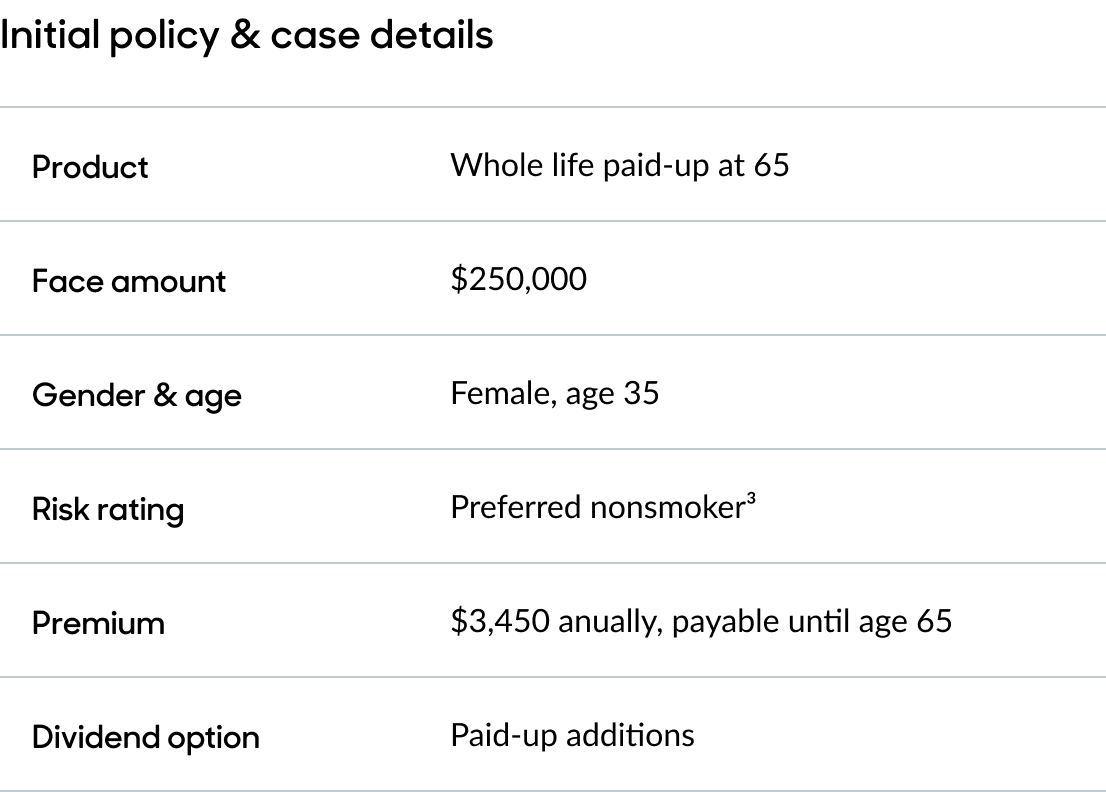

After learning the basics about PUAs, your clients may be wondering about the value they could provide over time. The comparison below of guaranteed vs. actual policy values for a whole life policy issued by MassMutual to a hypothetical insured in 19952 can help you demonstrate the real power of PUAs.

The results shown reflect the actual experience of the company during this time period, primarily with respect to investment results, mortality, and expenses. Dividends paid in future years will be lower or higher than illustrated, depending on MassMutual's operating experience over time.

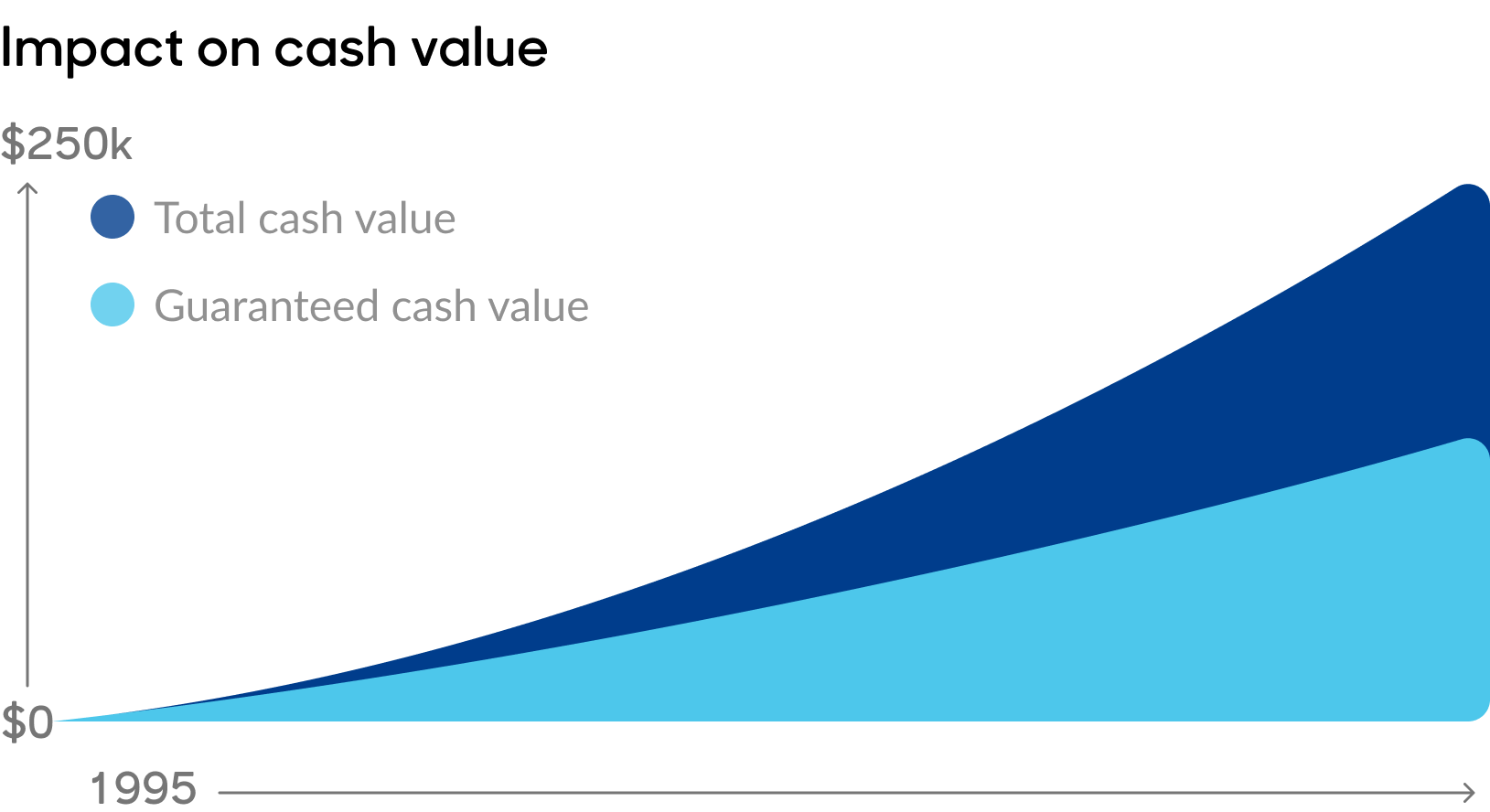

This chart compares the policy cash value that was guaranteed in 1995 to the actual total policy cash value results through 2026. This includes the base policy cash value and the cash value of accumulated paid-up additions.

By 2026, the guaranteed cash value is $136,858. The total cash value is $249,908. The PUAs that the policy has received has resulted in this nearly 83% increase in cash value.

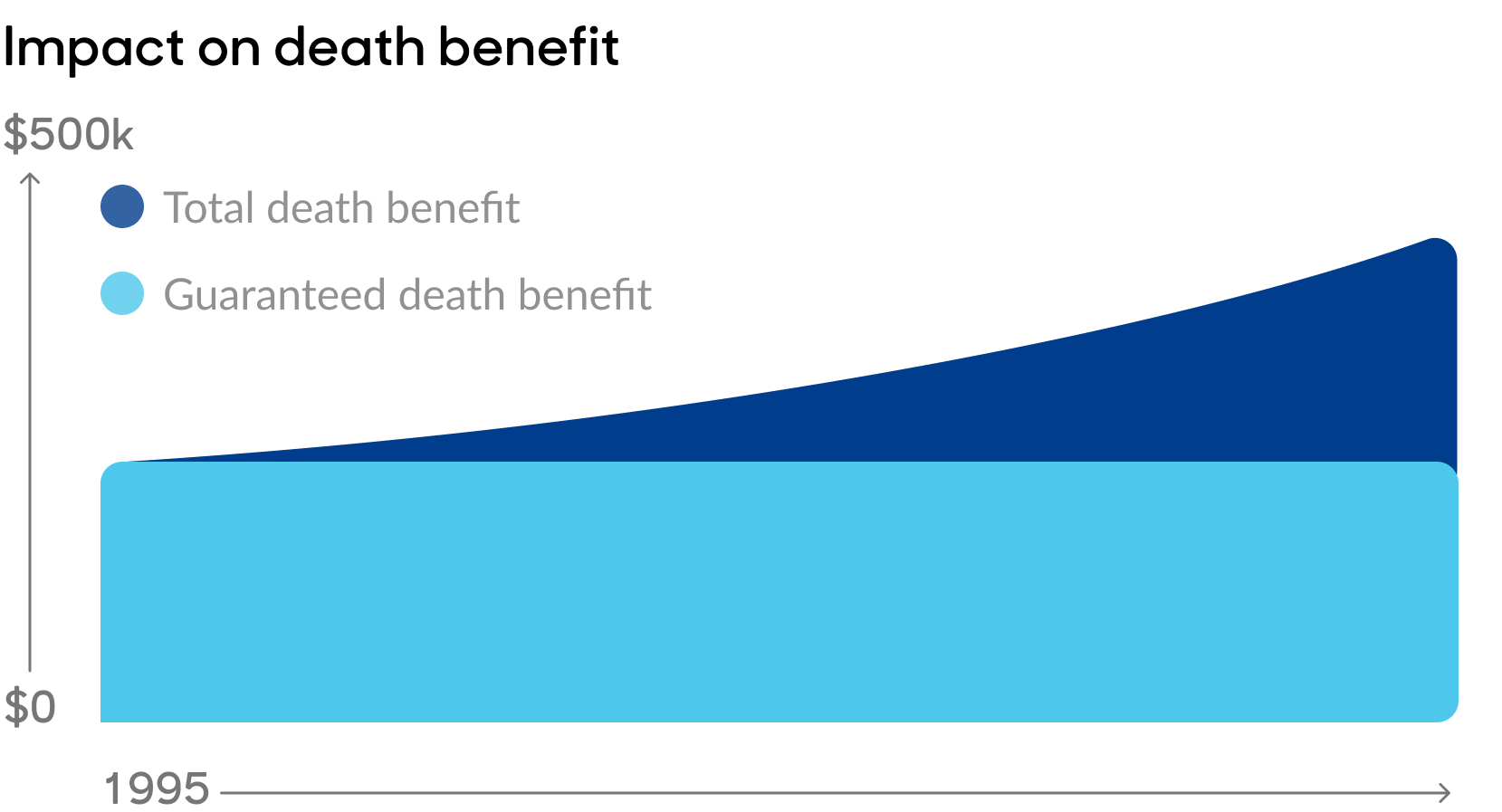

This chart compares the policy death benefit that was guaranteed in 1995 to the actual total policy death results through 2026. This includes the base policy death benefit and the death benefit accumulated paid-up additions.

The guaranteed death benefit of the policy is $250,000. By 2026, the total death benefit has increased to $456,511. This nearly 82% increase is because of the additional death benefit that the PUAs have purchased.

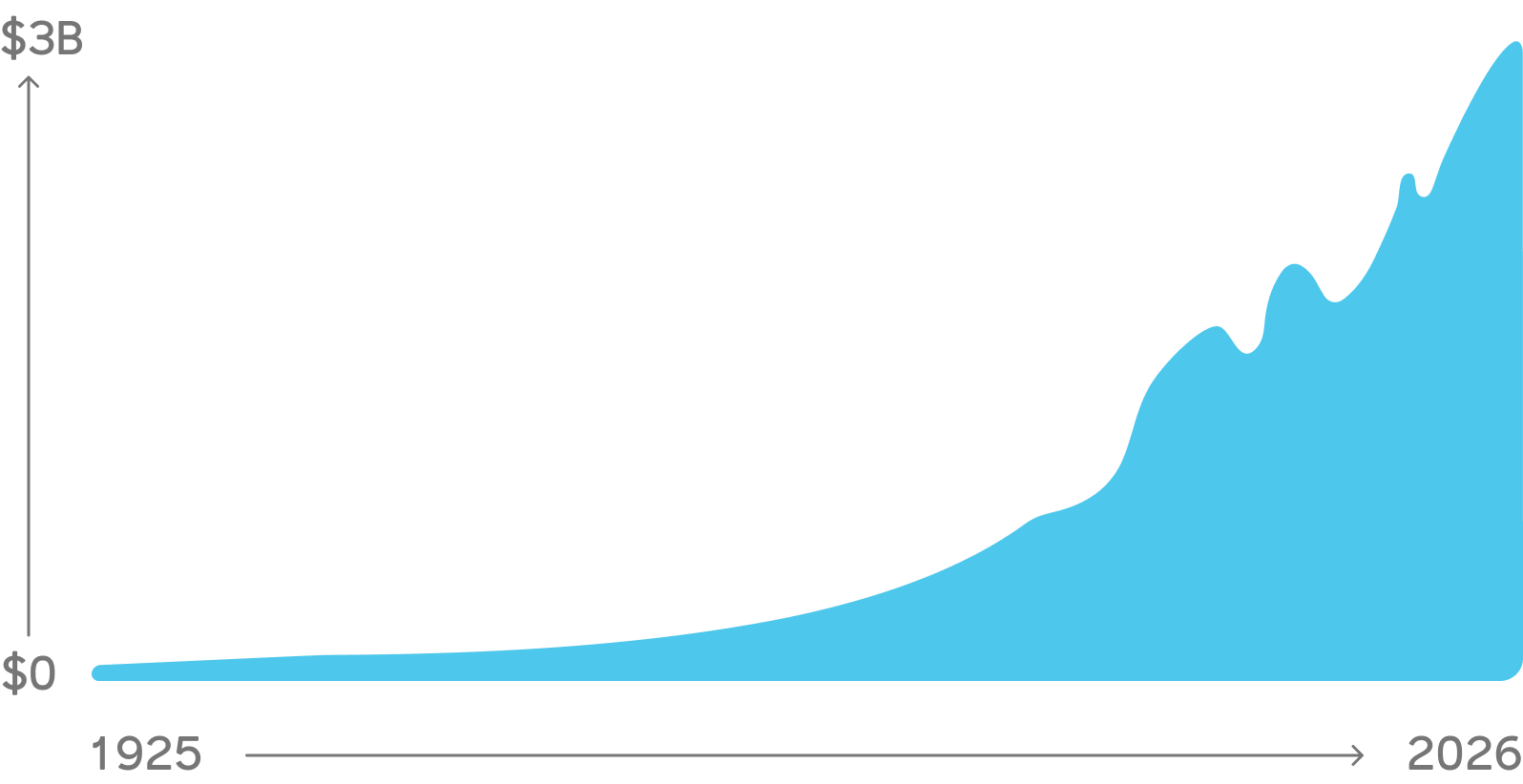

Consistently strong, historical results

As mentioned previously, while dividends are not guaranteed, MassMutual has a strong track record of paying them to eligible participating policyowners. In fact, dividends have been paid every year since 1869.

$2.9B

Estimated dividend payout in 20254

158 years

Of consecutive annual dividend payments to participating policyowners

6.60%

Dividend interest rate (DIR) in 20264

20 years

Of industry-leading DIRs among core mutual competitors

FOR FINANCIAL PROFESSIONALS. NOT FOR USE WITH THE PUBLIC.

1 Distributions under the policy (including cash dividends and partial/full surrenders) are not subject to taxation up to the amount paid into the policy (cost basis). If the policy is a Modified Endowment Contract, policy loans and/or distributions are taxable to the extent of gain and are subject to a 10 percent tax penalty if the policyowner is under age 59½.

2 This policy was issued by MassMutual prior to the merger with the former Connecticut Mutual Life Insurance Company in 1996. Policies in this block of business are no longer available for purchase. The policy was issued with an adjustable loan rate.

3 Preferred Nonsmoker was the best risk class available for this policy series. This risk class is no longer available.

4 The dividend and dividend interest rate (DIR) are determined annually, subject to change and are not guaranteed. Dividends for eligible participating life insurance policies primarily consist of investment, mortality and expense components. The DIR is used to determine the investment component of the dividend. It is not the rate of return on the policy and should not be the sole basis for comparing insurers or policy performance.

The products and/or certain features may not be available in all states. State variations will apply.

Participating whole life insurance policies issued by Massachusetts Mutual Life Insurance Company (MassMutual), and its subsidiary, C.M. Life Insurance Company, Springfield, MA 01111-0001.