Tax advantages of Whole Life Insurance

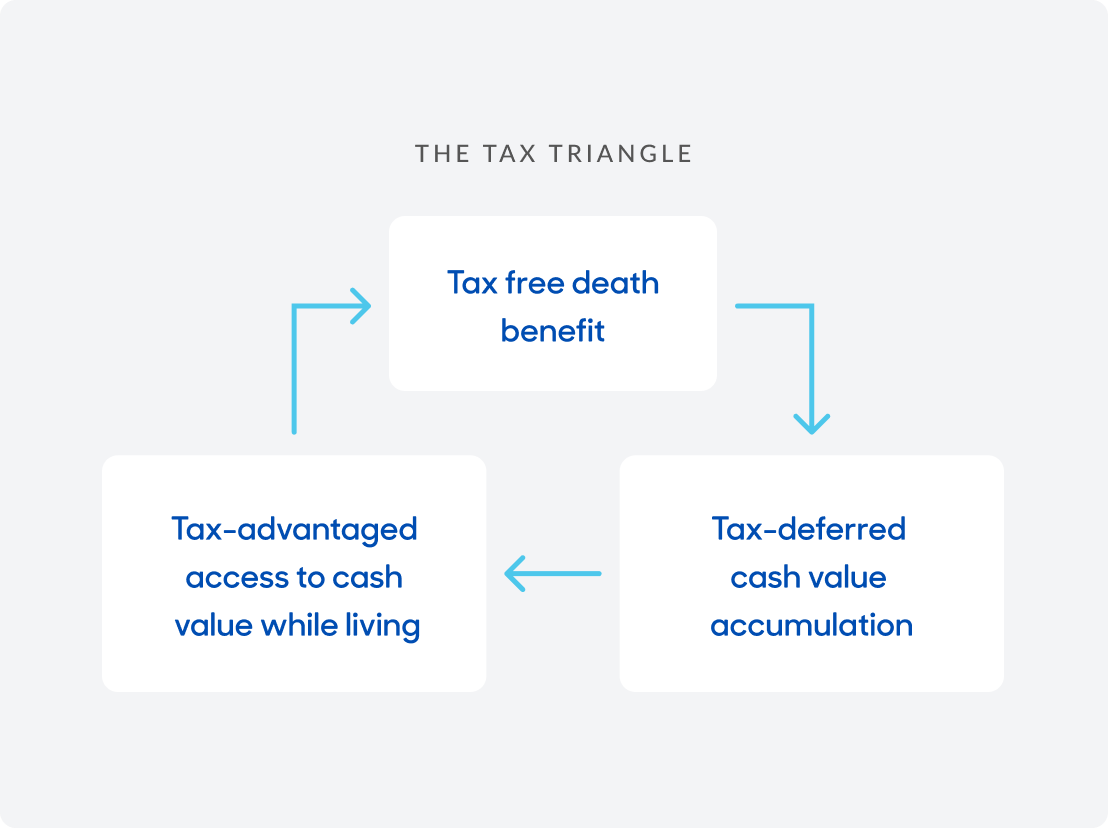

When it comes to wealth, there are generally three account types that funds can be held in– taxable, tax-deferred, and tax-advantaged. These are commonly known as the tax triangle.

While the primary purpose of a whole life policy should be to provide insurance protection that continues for life, it can also be leveraged to build financial strategies that offer diversified tax benefits. Whether helping clients to build an estate or wealth transfer plan, secure their financial future, or address their retirement concerns, there are many ways that permanent life insurance coverage can help.

Integrating whole life insurance into a financial strategy offers the following tax advantages:

- Tax-free death benefit

- Tax-deferred cash value accumulation

- Tax-advantaged access to cash value while living

Learn more about the tax triangle (PDF)

Learn more about income taxation of whole life insurance (PDF)

Consider what MassMutual Whole Life has to offer

Whole life insurance is a powerful financial tool that can support a variety of financial strategies over the course of your clients’ lifetime, while offering significant tax advantages. MassMutual Whole Life is no exception, delivering powerful benefits to help secure the financial future of clients and their loved ones.

Learn more about income taxation of whole life insurance (PDF)

Income tax free death benefit

One of the most important components of whole life insurance is the tax-free death benefit, which beneficiaries receive without paying federal income taxes upon the insured's death, making it an effective estate and wealth transfer planning tool that can help preserve wealth and minimize tax impact for future generations.

Tax-deferred cash value accumulation

The cash value of a whole life policy accumulates on a tax-deferred basis, meaning no taxes are required as the cash value increases. The available cash value may be used for any reason1, during working years, to help with college expenses, or to supplement income in retirement, offering financial flexibility as a living benefit of the policy.

Tax-advantaged access to cash value

Whole life insurance policies also offer the ability to access the available cash value in a tax-advantaged manner via partial surrenders or policy loans without triggering an immediate tax liability.1 This makes these policies an appealing option to consider when supplementing a retirement income strategy.

The decision to purchase life insurance should be based upon long-term financial goals and the need for death benefit. Life insurance is not an appropriate vehicle for short-term savings or short-term investment strategies. While the policy allows for loans, you should know that there may be little to no cash value available for loans in the policy’s early years.

The information provided is not written or intended as specific tax or legal advice. MassMutual, its subsidiaries, employees and representatives are not authorized to give tax or legal advice. Individuals are encouraged to seek advice from their own tax or legal counsel.

Call us to learn more

Talk to our knowledgeable financial professionals about how life insurance strategies and solutions can meet your client needs at 1-413-744-1202 or find your Managing Director.

FOR FINANCIAL PROFESSIONALS. NOT FOR USE WITH THE PUBLIC.

1 Distributions under a whole life insurance policy (including cash dividends and partial/full surrenders) are not subject to taxation up to the amount paid into the policy (cost basis). If the policy is a Modified Endowment Contract, policy loans and/or distributions are taxable to the extent of gain and are subject to a 10% tax penalty if the policyowner is under age 59 ½.

Access to cash values through borrowing or partial surrenders will reduce the policy’s cash value and death benefit, increase the chance the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured.

The products and/or certain features may not be available in all states. State variations will apply.

MassMutual Whole Life series policies (Policy Forms: MMWL-2018 and ICC18-MMWL in certain states, including North Carolina, and MMWLA-2018 and ICC18-MMWLA in certain states, including North Carolina) are level-premium, participating, permanent life insurance policies issued by Massachusetts Mutual Life Insurance Company (MassMutual), Springfield, MA 01111-0001.